“FY25 was truly a transformational year for Fino,” MD and CEO Rishi Gupta said at the beginning of Fino Payment Bank’s earnings call for Q4 FY25.

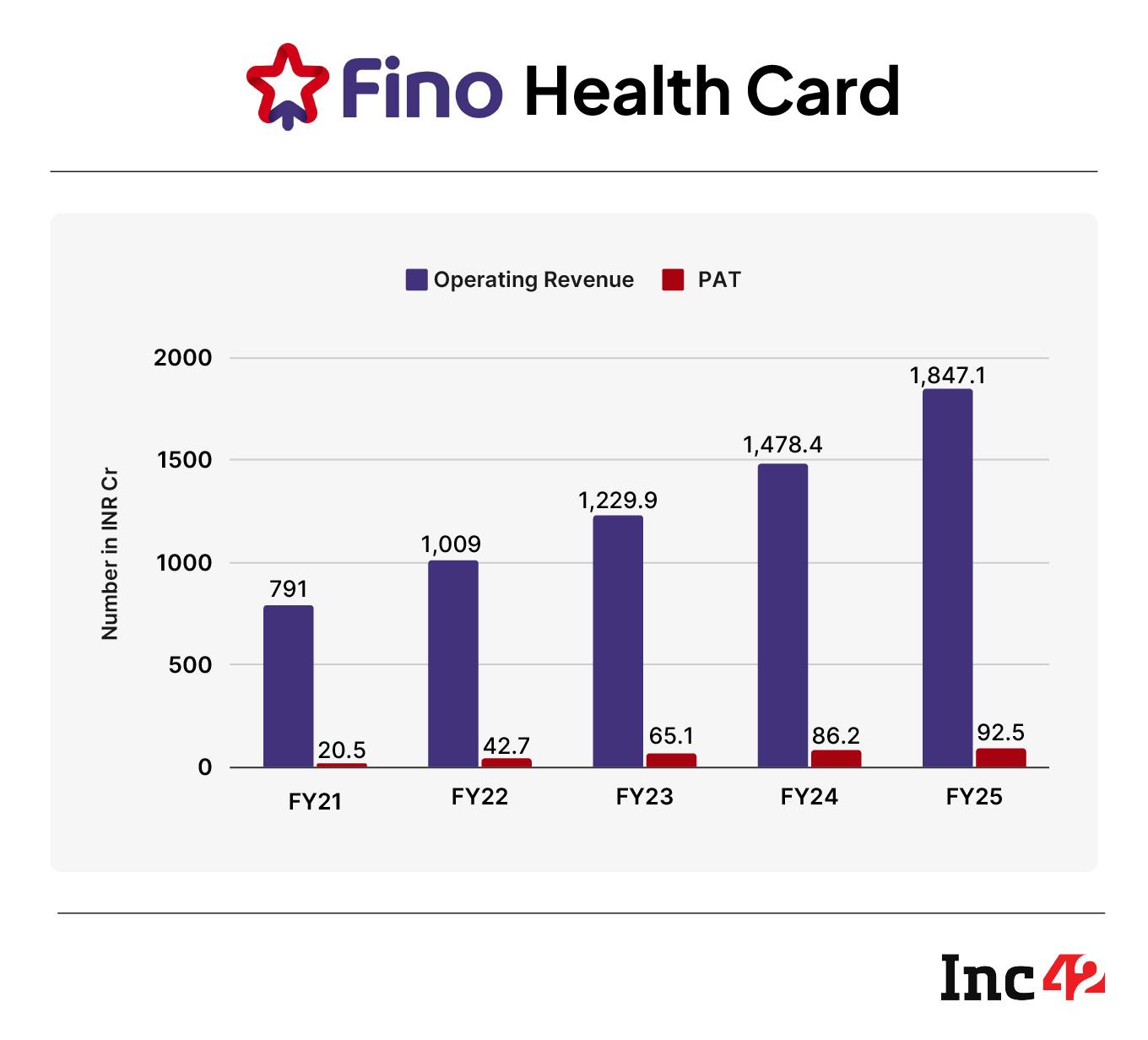

Registering its fifth consecutive profitable fiscal, the payments bank posted a net profit of INR 92.5 Cr in FY25, up 7% YoY. The company registered a 25% YoY increase in its top line, reporting a total revenue of INR 1,847.1 Cr.

While its top-line growth was in line with its guidance for the fiscal year, taxes took a toll on its profitability. Notably, the bank became a tax-paying entity in Q2 FY25.

Speaking with Inc42, CFO Ketan Merchant said that the payments bank is now targeting a 20-25% growth in its FY26 top line. The bank, however, expects its profit before tax (PBT) to remain flat at 5.9%, similar to what it had recorded in FY25. The cost-to-income ratio is projected to stay near 25%, also consistent with the FY25 levels.

Outlining the bank’s focus for the current fiscal, Merchant said, for Fino, which he believes has been known as a bank for the blue-collar workforce, the focus will see a slight shift to targeting slightly above the mass-market consumers.

Giving a lowdown on the company’s FY26 strategy, the CFO said that Fino Payments Bank’s primary growth levers for the ongoing fiscal year will be digital transactions and CASA expansion.

Besides, the bank plans to deepen its product offerings, introduce corporate digital payment tools, and maintain profitability while operating within existing geographies.

New Product Launches To Support Digital GrowthCurrently, Fino Payments Bank offers UPI services such as QR codes, credit cards on UPI, UPI Lite, and UPI Circle (a feature that allows a primary UPI user to authorise a secondary user to make transactions from their account), among other standard UPI offerings.

Digital transactions comprised 49% or INR 2.25 Lakh Cr out of a total throughput of INR 4.6 Lakh Cr. This marks a big shift from FY19, when 99% of the throughput came solely from its physical channels.

The bank attributes the growth in digital transactions largely to the business-to-business (B2B) merchant segment. The CFO, however, noted that any significant shift in merchant behaviour could affect this trajectory.

To support its digital growth, Fino plans to launch a UPI-based bulk payment product called “Payout” in FY26. The product will target corporate clients who make high-volume payments to multiple recipients.

“This will help us deepen our digital B2B footprint,” the CFO noted, adding that the launch is expected in Q2 FY26.

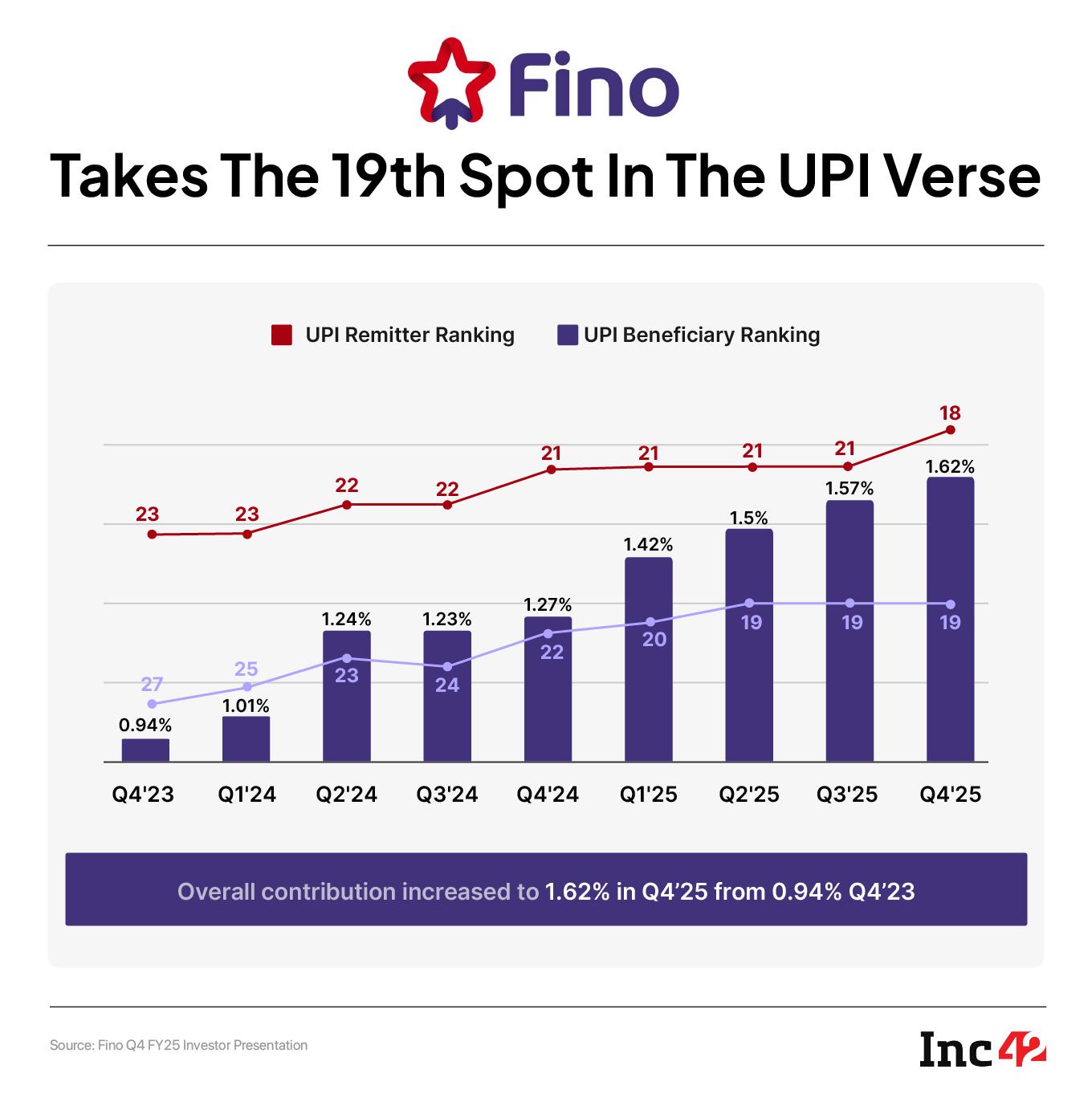

Meanwhile, CEO Rishi Gupta said its UPI market share increased from 1.27% in Q4 FY24 to 1.62% in Q4 FY25. With this, digital has become a central part of the bank’s transaction account monetisation (TAM) strategy, which it has been following for the past three years.

Merchant said that digital business margins are currently at a gross margin level of 21–22%, with profit-before-tax (PBT) margins exceeding 10%.

Meanwhile, technology investments are expected to continue in FY26, with a projected capital expenditure of INR 90-100 Cr. In FY25, the bank spent INR 165 Cr on core banking system migration.

Increased Focus On CASAThe bank will be increasing its focus on the CASA (current accounts and savings accounts) segment, which it identifies as a key growth area. In FY25, Fino launched a CASA product, Gullak, for MSME employees and blue-collar workers.

According to the bank, the product helps generate annuity-based income, with 65% of customers renewing into their second and third years. The bank is planning to launch a similar product for a slightly higher-income consumer. This is part of Fino’s strategy to expand its CASA offerings to include products designed for customers with higher average balances.

“The current average CASA balance is INR 1,300. We are now working on new offerings for customers with balances of INR 5,000 and above. These will be aimed at customers in tier II and III cities,” Merchant said.

Replying to a question about the bank’s expansion to newer locations, he said the bank is not planning to expand to new geographies but instead intends to increase its penetration among middle-income customers in the same markets.

Fino does not plan to compete directly with private sector banks but wants to grow gradually in India’s middle-income segment.

However, Transition To Small Finance Bank Is InevitableOne of Fino’s goals in the ongoing financial year is to transition to an SFB (small finance bank). The move will allow it to add lending capabilities to its existing asset-light payments bank model. The bank had with the Reserve Bank of India (RBI) in January 2024.

Under its SFB model, Fino will sharpen its focus on customer deposits, including those in savings and checking accounts, using its existing distribution network and tech infrastructure.

As of now, the bank is working with regulators to introduce loan referral services and a prepaid payments vertical.

Its SFB model will comprise limited physical branches. It would selectively partner with fintech platforms. However, this transition will include continued investment in core technology infrastructure. This would increase Fino’s expenses in FY26. Merchant anticipates an additional capex of INR 90 Cr to INR 100 Cr for running its SFB.

As part of the transition, Fino plans to increase engagement with existing merchants by offering multiple services rather than focussing solely on new acquisitions. The bank is also working on simplifying the onboarding process for new customers.

A significant part of the FY26 strategy involves shifting from assisted or cash-based behaviour to digital self-service platforms.

Platform activity for its UPI offering is expected to grow. The company’s digital transaction volume grew 80% from INR 160 Cr in FY24 to INR 288 Cr in FY25. The bank also aims to use this platform momentum to support recurring revenue streams.

As Fino Payments Bank gears up for its next phase of growth, the roadmap for FY26 is clear — deepen digital engagement, broaden CASA base, and transition into a small finance bank. However, it will need a steady focus on profitability, capital efficiency, and product innovation. Can it stay on course?

(Edited by: Shishir Parasher)

The post appeared first on .

You may also like

Iran foreign minister takes first strike in Pakistan as 'mediator', to land in Delhi today

Arsenal can use PSG Champions League showdown to help Mikel Arteta push £17m summer transfer

Emmerdale's Lewis Barton actor teases huge 'secret' he's keeping from Ross

Emma Raducanu 'nervous' about failing drugs tests and fears being targeted

Omar Abdullah, Mehbooba Mufti question 'mass detentions' after Pahalgam attack